Pervasive Artificial Intelligence Research (PAIR) Labs

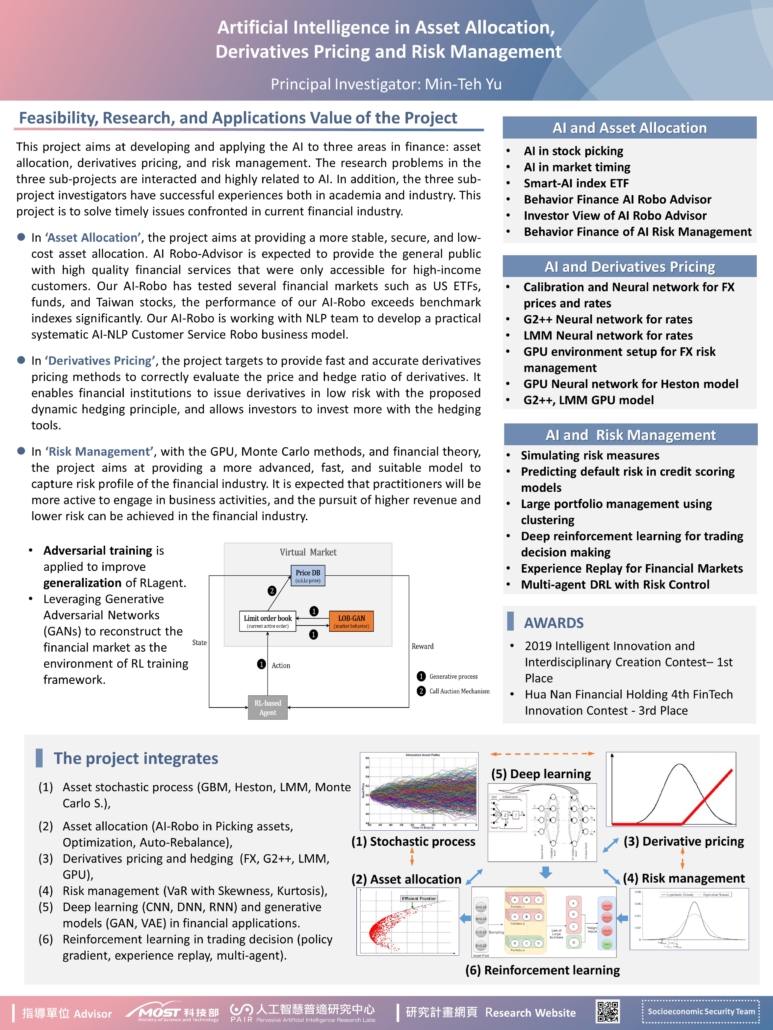

Artificial Intelligence in Asset Allocation, Derivatives Pricing and Risk Management

Principal Investigator: Professor Min-Teh Yu

Summary

This project was proposed in response to the Ministry of Science and Technology (MOST) for promoting the development of various AI innovation research centers. The project applies various AI technologies in asset allocation, derivatives pricing and risk management. The first focus of this project is on how to form a high- yield portfolio and control the portfolio risks using AI. This projects applies GPU and financial theory to provide a more advanced model for capturing the risk profile of the financial assets, markets and institutions. A stable, secure and low-cost asset allocation AI Robo-advisor will be designed. The project also uses AI to develop fast and accurate derivatives pricing models for financial institutions, which can correctly evaluate the price and hedge ratio of derivatives. We also explore how Monte Carlo simulation with GPU can enhance the pricing and risk management for derivatives.

Keywords

Artificial Intelligence; Machine Learning; Portfolio Management; Trading Strategy; Stock Picking; Market Timing; Smart-AI Index ETF; Stochastic Volatility; Derivatives; Options; Market Calibration; Graphics Processing Unit; Compute Unified Device Architecture; Economic Scenario Generator; Risk Management; Monte-Carlo Simulation; Value at Risk; Expected Shortfall.

Innovations

- Evaluate the stock picking and market timing strategies using machine learning techniques with corporate and market data. It then applies the machine learning methods to predict future states of the economy and stock market using macroeconomic variables to develop a smart-AI index ETF.

- Propose a spherical Monte Carlo estimator and a simple importance sampling scheme to improve the efficiency of the spherical Monte Carlo in calculating risk measures and prices. It also considers asset allocation and credit risk prediction with machine learning techniques.

- Develop a multi-agent based deep reinforcement learning framework with a two-level nested agent structure to learn effective portfolio management. It also proposed a specially designed reward function for investment performance evaluation and a novel policy network structure for trading decision making to construct a model, which can optimize multi-period portfolio management with realistic transaction cost.

- Integrate financial engineering model, behavioral finance theory, and various types of neural network algorithms of AI to construct a set of stochastic process models and estimate model parameters under AI. It then computes VaR by Monte Carlo simulation under GPU computing to build a risk management model that reflects the true risk profiles of financial institutions.

- Apply the CUDA (Compute Unified Device Architecture) of NVIDIA to resolve the computational complexity of Monte Carlo simulation to produce timely price and risk measures for a large portfolio of assets and liabilities of financial institutions.

- Provide timely measures of value at risk, expected shortfall, BIS Ratio for banks, and Solvency II ratio for insurance companies using AI-assisted derivatives pricing models with GPU parallel computing.

Benefits

This project aims at developing and applying the AI to three areas in finance: asset allocation, derivatives pricing, and risk management. The research problems in the six sub-projects are interacted and highly related to AI. In addition, the six sub-project investigators have successful experiences both in academia and industry. This project is to solve timely issues confronted in current financial industry.

- In ‘AI’ and ‘Derivatives Pricing’, the project is targeted to provide fast and accurate derivatives pricing methods to correctly evaluate the price and hedge ratio of derivatives. It enables financial institutions to issue derivatives in low risk with the proposed dynamic hedging principle, and allows investors to invest more with the hedging tools. Mutually, it is expected that the economy will become more prosperous.

- In ‘AI’ and ‘Risk Management’, with the GPU and financial theory, the project aims at providing a more advanced, fast, and suitable model to capture risk profile of the financial industry. It is expected that practitioners will be more active to engage in business activities, and the pursuit of higher revenue and lower risk can be achieved in the financial industry.

- In ‘AI’ and ‘Asset Allocation’, the project aims at providing a more stable, secure, and low-cost asset allocation. AI Robo-Adviser is expected to provide the general public with high quality financial services that were only accessible for high-income customers.

{kind=link}